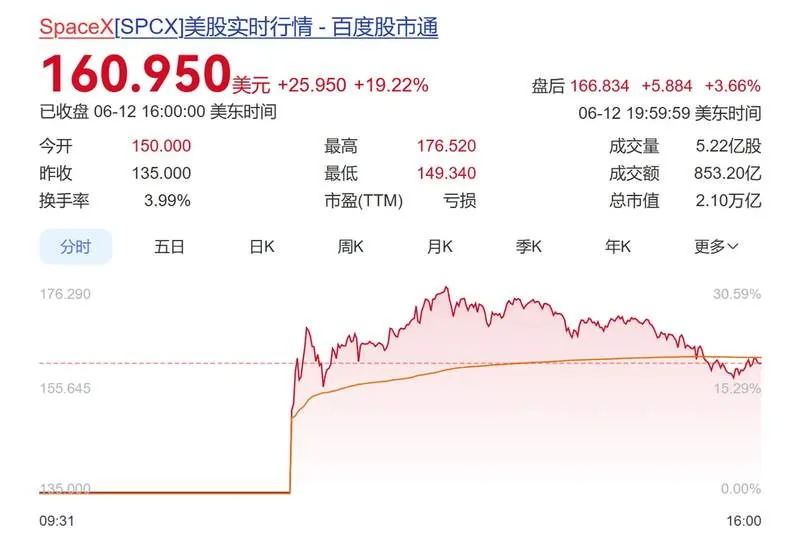

China's Mega-IPO: Dream Cradle or Wreckage?

The Chinese internet has a special phrase for projects that begin with grand promises and end in rubble: 烂尾工程 — literally "unfinished project." Originally coined for abandoned construction sites — half-built apartment towers, incomplete bridges, forgotten theme parks — it's now the ultimate insult in the Chinese tech vocabulary.

So when a Toutiao (今日头条) headline trending at 3.4 million engagement asks whether "the largest IPO in history" is a "cradle of dreams" (造梦摇篮) or an "unfinished project" (烂尾工程), the cultural temperature has clearly shifted. This isn't celebration. This is the Chinese internet doing what it does best: smell-testing the hype.

Let's be real about what's happening. China's tech IPO market in 2025 is a strange, twitchy beast. After years of regulatory winter, the freeze is thawing — but investors are battle-scarred and deeply suspicious. They've been burned before.

Remember when Ant Group (蚂蚁集团) was going to be the largest IPO in history back in 2020? That $37 billion dual-listing was yanked two days before trading. Poof. Gone. The "largest IPO ever" became the largest IPO cancellation ever. Chinese investors have long memories and they hold grudges.

Now, whenever a company pitches itself as the next mega-listing, the default reaction isn't excitement — it's forensic skepticism. The Toutiao headline captures this perfectly: is this a dream factory or another wreck in progress?

This skepticism is baked into Chinese consumer internet culture right now. After a decade of hyper-growth narratives — "blitzscale everything," "burn money to monopoly," "platform economy forever" — Chinese netizens have developed a bullshit detector so sensitive it could register a VC's elevator pitch from three WeChat groups away.

They've watched the carnage:

- DiDi (滴滴) — pulled its app from stores immediately after its US IPO. Investors annihilated.

- Kuaishou (快手) — stock cratered 80%+ after its 2021 Hong Kong debut.

- Pop Mart (泡泡玛特) — rode the blind-box wave, then faced existential questions about whether its model was sustainable or just a beautifully packaged fad.

- Countless smaller listings that promised Mars and delivered a studio apartment in Shijiazhuang.

The "造梦" (dream-making) framing matters. In Chinese internet culture, this has a very specific flavor — it's the art of selling a vision before the product exists. Think "selling the dream" with Chinese characteristics and a 996 work culture. Every major platform has done it: WeChat (微信) sold the dream of universal connection; Douyin (抖音) sold the dream of everyone-becomes-a-creator; Pinduoduo (拼多多) sold the dream of cheap-everything-delivered-tomorrow.

But when IPOs get labeled as "dream-making," Chinese investors now ask the uncomfortable question: what happens when the dream meets spreadsheet reality?

The "烂尾" metaphor is devastating precisely because it strips away the tech-sector gloss. An unfinished building isn't "disruptive" or "innovative" — it's just incomplete. A monument to overpromising. When you call a potential IPO a "烂尾工程," you're essentially saying: this might be a beautifully marketed scam.

What's fascinating is how this plays out across sectors:

AI companies are especially vulnerable. DeepSeek (深度求索) shocked the world and became a national pride moment — but now every Chinese AI lab wants IPO darling status. Qwen (通义千问), Doubao (豆包), Kimi (月之暗面), Zhipu (智谱) — they're all positioning. But which are building real businesses versus incinerating venture capital? Investors are deploying the "烂尾 test": will these companies deliver revenue, or become expensive research projects with no monetization?

Robotics is even more speculative. Unitree (宇树科技) makes stunning humanoid robots. Fourier (傅利叶) has its GR-1. Agibot (智元) is raising at eye-watering valuations. But commercial viability remains a question mark. The gap between viral demo videos and actual paying customers is exactly where IPO dreams go to become 烂尾 nightmares.

Consumer platforms face the inverse problem — they have users but exhausted growth narratives. Xiaohongshu (小红书) keeps teasing IPOs. Meituan (美团) is public but fighting multiple fronts simultaneously. Bilibili (B站) has struggled with profitability questions for years. The issue isn't whether they have audiences — it's whether growth stories survive in a saturated market.

The cultural backdrop is essential here. Chinese consumers and investors have ridden a rollercoaster. The "involution" (内卷) discourse, the "lying flat" (躺平) movement, genuine economic headwinds — all of it has created a population significantly less willing to buy grand narratives from people in Patagonia vests.

When Toutiao users see "largest IPO in history," they don't see opportunity. They see flashing warning signs. They see ghosts of listings past. They remember colleagues who lost savings on tech stocks, startups that vanished overnight, promises that evaporated faster than a livestream commerce ban.

This is healthy skepticism, and it's fundamentally reshaping how Chinese companies approach public markets. The "list first, figure out profits later" era is dying a well-deserved death. Investors now demand:

- Real revenue, not vanity GMV

- Actual margins, not "we'll monetize later"

- Clear regulatory positioning (non-negotiable in Xi-era China)

- Shipped products with users, not polished pitch decks

The Toutiao headline isn't about one IPO — it's a referendum on the entire Chinese tech IPO model. Are these companies building durable value, or selling Lotus-eater dreams to institutional investors planning to dump on day one?

For the global audience watching China's tech sector: take notes. When you see breathless Western coverage of "China's next mega-IPO," remember that Chinese netizens have already asked the hard questions and found the hype wanting. They're not buying what's being sold. They've been burned too many times by too many "game-changers."

The smartest Chinese companies understand this. They're not selling dreams — they're showing receipts. DeepSeek didn't hype itself toward an IPO; it released a model that worked and let the results speak. Pop Mart built actual retail infrastructure before listing. The lesson is clear: in 2025 China, you can't just be a "dream cradle." You have to deliver the dream fully assembled.

Otherwise? You're just another 烂尾工程 with better branding.